StonebridgeFOCUS – Tax Outlook for 2019: Four Things to Know Before April

It’s been more than a year since Congress passed, and President Trump signed, the Tax Cuts and Jobs Act of 2017. In the time since, Trump met with North Korean leader Kim Jong-un, the US imposed $34 billion in tariffs on Chinese goods, the Democrats retook the House of Representatives, the equity markets had their worst week since the 2008 Global Financial Crisis, France won the World Cup, Saudi Arabia allowed women to drive, and Prince Harry married Meghan Markle.

All of which is to say that you could be forgiven if a tax law from 2017 hasn’t exactly been at top of your mind. However, here’s the thing: Even though the bill became law in December 2017, most of its provisions didn’t apply to the 2017 tax year. Which means the 2018 tax year—the very taxes we’ll all be filing come April—will be the first time we’ll have to truly grapple with the new law. What might it mean for investors? And what’s the outlook for investment taxes in 2019?

Recently, Parametric Portfolio Associates published a Research Commentary entitled, “2019 Tax Outlook for Investors: Everything Old is New Again,” which we thought would be of interest.

In brief:

- Lower tax rates on income, interest, and short-term capital gains.

- No change to long-term capital gain and dividend tax rates.

- Reductions in tax rates are modest and not universal, continuing to make active tax management extremely valuable.

There’s a lot that’s new, from the widely applicable (revised individual income brackets) to the fairly arcane (a tax cut for citrus growers). But for the purposes of this blog post, let’s focus on just four key provisions affecting investors.

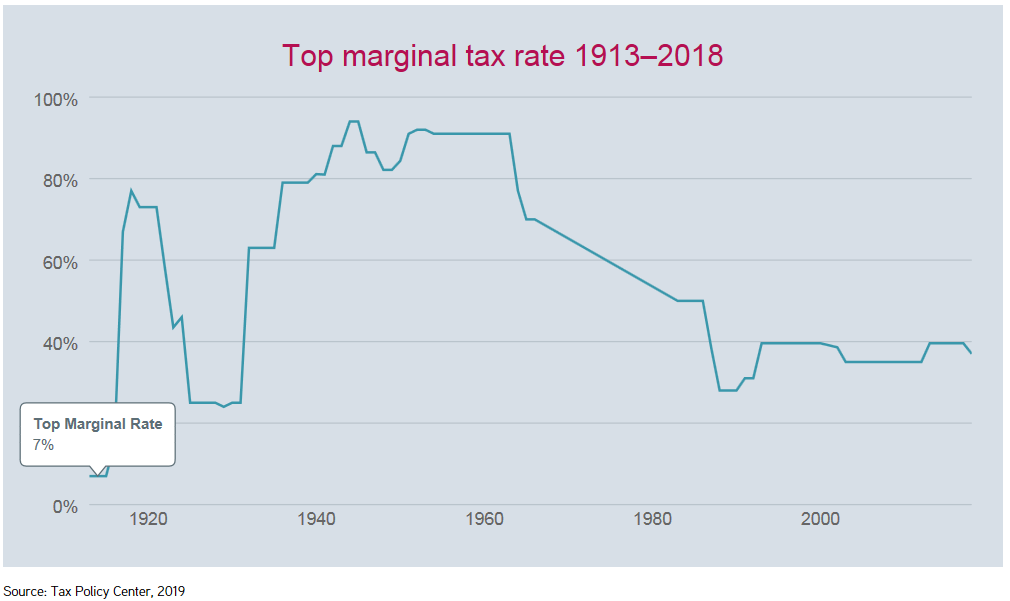

Lower tax rates on income, interest, and short-term capital gains

For 2018 through 2025, the law lowers income tax rates for most individuals, with the top rate down to 37% from 39.6%. These are the rates that apply to interest income and realized short-term capital gains or losses. Adding in the 3.8% tax on investments from the Affordable Care Act (ACA), the highest federal bracket will be 40.8% instead of 43.4%. For investment portfolios set up as trusts or pass-through entities, the tax rates may be even lower. However, deductions for state and local taxes have been limited, so in some cases investors may see an increase in their effective tax rate.

What it means for you: For many investors, a lower tax rate will mean increased after-tax performance in their investment portfolios. However, reductions in tax rates are modest and not universal, continuing to make active tax management extremely valuable.

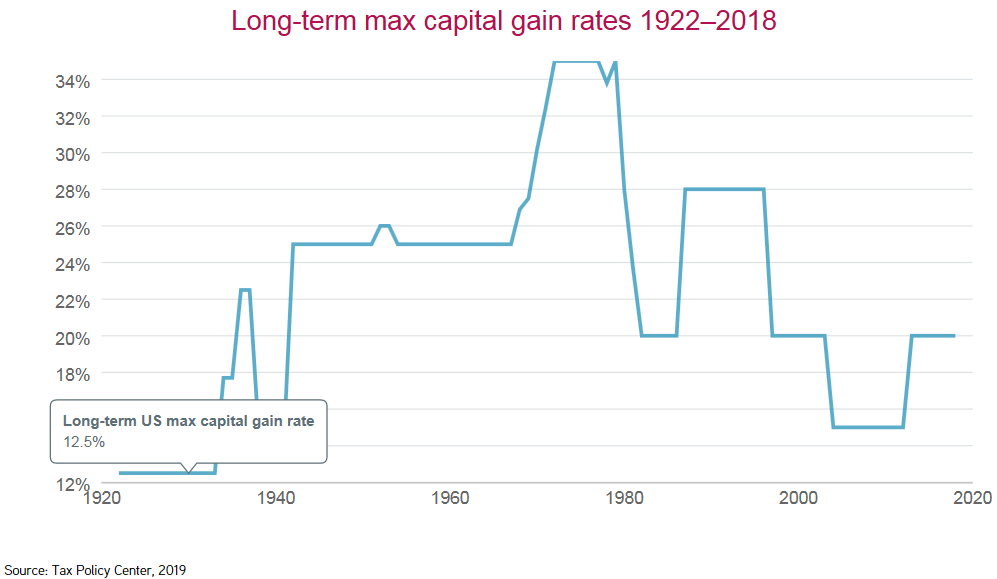

No change to long-term capital gain and dividend tax rates

The tax act retains the existing 0%, 15%, and 20% brackets on long-term capital gains and qualified dividends. With the 3.8% tax from the ACA, the highest bracket is 23.8%.

What it means for you: There’s still a large difference between the short-term gain rates and the long-term gain rates. A key strategy for tax management still applies: Investors should avoid short-term gains, realize short-term tax losses, and defer long-term gains as long as possible.

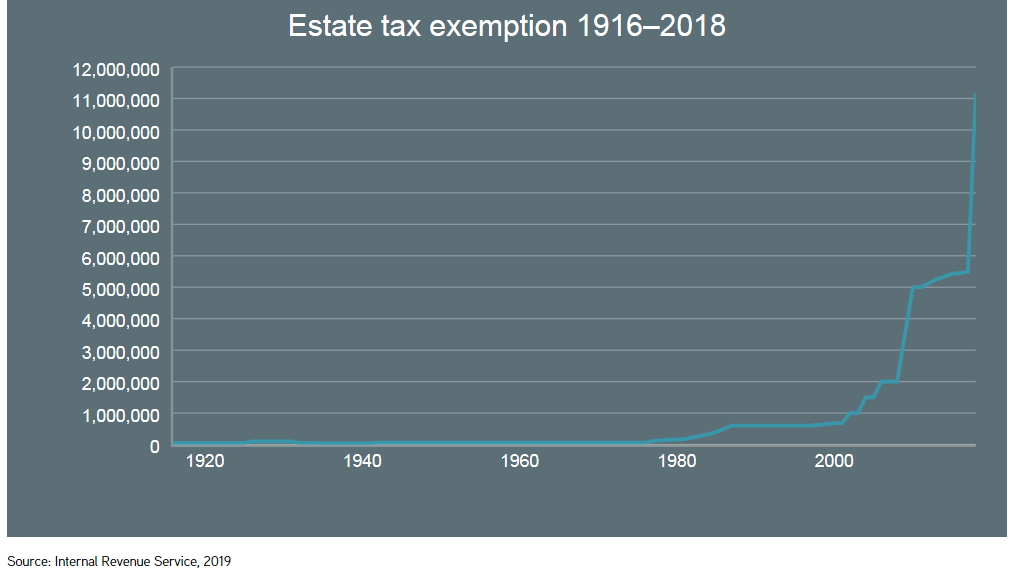

The estate tax exemption has doubled

The estate tax exemption doubles for those estates realized between 2018 and 2025, from just over $5 million to more than $11 million for an individual. The step-up in cost basis of the assets at death is preserved in the new law. Charitable deductions are still allowed for those that itemize (but note that the standard deduction has also doubled, so taxpayers will need to clear a taller hurdle to claim charitable deductions on their taxes).

What it means for you: Fewer taxpayers will need complicated tax planning for their estates. Investors can defer tax liability into the future, realize the tax liability at the long-term rate, give away the liability by selecting the optimal tax lots for charitable giving, or simply let the tax liability expire with the step-up in basis that occurs when the estate is realized.

AMT is still alive, but it will apply to fewer taxpayers

The alternative minimum tax (AMT) now affects only those taxpayers at higher income levels. Also, while under the old law many taxpayers triggered AMT with deductions for state and local taxes and property taxes, new limitations on those deductions means AMT will be harder to trigger.

What it means for you: From an investor’s tax-management perspective, AMT has a negligible effect.

What could change for investors in tax year 2019?

With a divided Congress the chances of any major tax legislation getting through either chamber appears slim. In the days leading up to the 2018 midterm elections, there was talk of a middle-class tax cut, an idea Democrats have also embraced more recently, but in this political climate it’s hard to see the two sides coming to agreement on exactly what that might look like.

There were also murmurs from the Trump administration in July 2018 of using an executive order to index capital gains to inflation, which would have been a huge boon for high-net-worth investors (but would have brought with it a host of other complex issues to resolve). That idea also went nowhere fast.

So from a tax perspective, will nothing change in 2019?

It’s very likely. But as fans of Seinfeld will tell you, there’s something to be said for nothing. For example, as Congress was negotiating the new tax law late in 2017, one proposal was to require investors to use a first in, first out (FIFO) accounting methodology for tax lots when calculating capital gains taxes. This would have caused capital gains taxes to go up and led to more assets stuck in concentrated portfolios instead of being appropriately diversified. Fortunately for investors, FIFO was left out of the final bill.

Our point of view

The new tax law may not truly be new anymore. Nevertheless, it presents investors with new complexities and opportunities for managing their taxes1.

“Believe me, all the billionaires I’ve ever met have one attribute in common: they and their advisors are really smart about taxes! They know that it’s not what they earn that counts. It’s what they keep. That’s real money, which they can spend, reinvest, or give away to improve the lives of others.”

-Tony Robbins

To learn more about our approach to active tax management and the importance of tax alpha, which we define as the excess return or value added by reducing taxes on a portfolio, please don’t hesitate to contact our team directly.

We look forward to continuing to provide useful insights and relevant solutions focused on helping you achieve your greatest financial potential.

Thank you for your continued trust and confidence in Stonebridge.

All the best,

Mitch

1Stonebridge does not provide tax advice. We recommend that you seek advice based on your particular circumstances from your business manager or independent tax professional.

About Parametric

Parametric Portfolio Associates LLC (Parametric) uses investment science to build and manage systematic investment strategies and to implement custom portfolio solutions providing clients with targeted investment exposures with control of costs and taxes. Based on principles of intellectual rigor, ingenuity and transparency, Parametric seeks to deliver repeatable client outcomes with consistently high levels of service and maximum efficiency. As of December 31, 2018, Parametric managed $216.6 billion in assets on behalf of institutions, high-net-worth individuals and fund investors. Headquartered in Seattle, Parametric also has offices in Minneapolis, Westport, Connecticut, Boston, and Sydney, Australia. For more information, visit parametricportfolio.com.

When Stonebridge decided to introduce an overlay portfolio management solution to its investment process, we chose to work with Parametric and SEI Private Trust Company. In the firm’s 2010 paper, Tax Efficient Investing in Theory and Practice, Parametric presented many of the concepts that now form the basis of Stonebridge’s tax alpha strategy; the added value by reducing taxes on an investment portfolio.