StonebridgeMARKETS | Coronavirus and Global Markets: What Investors Should Know

China reported an uptick in new cases of coronavirus known as “Wuhan flu,” “Wuhan coronavirus,” or nCoV on Friday, although the pace of increase was at its slowest since January, a downward trend that the World Health Organization (WHO) called encouraging. Although the WHO is working with Chinese officials and governments worldwide to contain nCoV, infections have been reported in 25 other countries. The epidemic is set to be discussed at a meeting of finance leaders from the Group of 20 major economies this weekend in Riyadh according to Reuters.

Recently, Natixis Investment Mangers published a market outlook entitled “Coronavirus and Global Markets: What Investors Should Know” which we thought would be of interest. A summary of the conclusions is provided below:

- The primary economic impact is driven by fear of infection throughout China, the world’s second largest economy and a major engine of global growth.

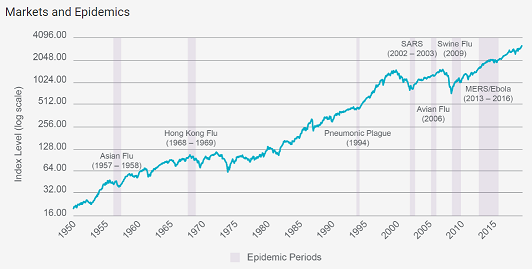

- Markets are likely to trade on headlines, which often skew negative. Looking at past pandemics, market weakness has proven to be short-lived with a sharp recovery in asset prices once evidence confirms that the outbreak has been contained.

- Earnings are what matter and the key indicators have been coming in quite strong with solid guidance.

Why should investors be concerned about coronavirus?

The primary economic impact is driven by fear of infection throughout China, the world’s second largest economy and a major engine of global growth. Transmission is a function of physical proximity to those infected, and China has experienced the vast majority of fatalities related to the disease.

nCoV originated in Wuhan, a city of approximately 8 million people located about 400 miles west of Shanghai within the Hubei province. Compared to other cities in China, the city is relatively small – Shanghai and Beijing are both home to over 20 million people. Nevertheless, nCoV is impacting behavior, with much of the public avoiding face-to-face contact. Business sentiment and consumer confidence are likely to be adversely impacted by contagion fears, eventually translating directly into the real economy. As a result, sectors like travel, tourism, entertainment, and hospitality are likely to be affected. Goods-producing industries and their related supply chains may be less affected, but will still likely endure some consequences of negative sentiment.

How does coronavirus compare to the outbreak of severe acute respiratory syndrome (SARS) in 2002–2003?

SARS impacted people of all ages, while nCoV seems to be most impactful on the elderly and those with existing conditions. Plus, the Chinese government has taken faster and more serious action to address nCoV as compared to the SARS outbreak. While SARS was first identified in November 2002 and not reported to the WHO until February 2003, nCoV was both first identified and reported to the WHO in December 2019. So far, nCoV also appears to have a lower fatality rate than SARS.

However, it is believed that nCoV has a longer incubation period than SARS, increasing the odds that the virus spreads undetected over time and location – and making the potential fallout more complex. Adding to this challenge, there is some evidence that some nCoV-positive cases present as asymptomatic, making detection that much more difficult.

Could the coronavirus outbreak be comparable to SARS in terms of negative economic impact?

It’s hard to say for sure – but it’s possible the negative economic impact of nCoV could be less severe. For one, retail sales today operate very differently than they did in 2003. Today, online sales are 20% of total sales – they were probably 0% of total sales during the SARS outbreak. The fact that fewer sales are done face-to-face could help insulate the public proximity concerns on the retail side. Technological innovations, e-commerce, and improved information technology (IT) and healthcare systems could also help limit nCoV’s economic effects. Ironically, the swift and aggressive measures taken by authorities to stem the rapid spreading of the virus relative to what was witnessed by SARS could prove to be more damaging economically than nCoV itself. Draconian quarantine measures taken by the Chinese authorities will certainly have an impact on the domestic economy. It appears their aim is to sacrifice short-term pain (sharp economic contraction) for long-term gain (quick recovery as virus is contained and widespread damage is limited). The locking down of entire cities and the imposition of strict travel restrictions will almost certainly grind local economies to a halt. What remains to be seen is how much this will have a spillover effect on the global economy.

Here, there is a key differentiating factor between nCoV and SARS. Back in 2003, China accounted for almost 4% of the global economy. Today, it is closer to 18%, over 4 times what it was 17 years ago. How long these preventive measures stay in place will be critical in determining the impact on both the domestic and global economy. We expect there will be significant efforts on the part of Chinese authorities to dampen the economic fallout of nCoV, including sizable liquidity injections, targeted financing, and a host of other measures aimed to support domestic demand and bolster the broader business sentiment.

Our Thoughts

Markets are likely to trade on headlines, which often skew negative. Looking at past pandemics, market weakness has proven to be short-lived with a sharp recovery in asset prices once evidence confirms that the outbreak has been contained. Encouragingly, data coming out of China tracking the virus indicates that the bulk of the new cases have been exclusive to the Hubei province and not spreading elsewhere. Importantly for the global economy, we have seen a lack of significant growth in cases contracted outside of China. Should these trends persist, the fear of contagion should subside, bringing a return of risk appetite back to the markets.

The nCoV outbreak was unexpected, but it comes at a time when many are calling for a market correction, given the impressive run in equity prices that ended 2019 and began 2020. The C makes for a perfect excuse for a pullback. However, markets have been impressively resilient so far. Assuming that the virus gets contained in the coming weeks, this does not change our bullish outlook. Earnings are what matter and the key indicators have been coming in quite strong with solid guidance.

“The stock market is a device for transferring money from the impatient to the patient.”

– Warren Buffet

To learn more about our distinctive goals-based approach to life and wealth management, please do not hesitate to contact our team directly.

We look forward to continuing to provide useful insights and relevant solutions focused on helping you achieve your greatest financial potential.

Thank you for your continued trust and confidence in Stonebridge.

All the best,

Mitch

About Natixis Investment Managers

Natixis Investment Managers serves financial professionals with more insightful ways to construct portfolios. Powered by the expertise of more than 20 specialized investment managers globally, we apply Active Thinking® to deliver proactive solutions that help clients pursue better outcomes in all markets. Natixis Investment Managers ranks among the world’s largest asset management firms3 with more than $1 trillion assets under management4 (€921.5 billion).

Headquartered in Paris and Boston, Natixis Investment Managers is a subsidiary of Natixis. Listed on the Paris Stock Exchange, Natixis is a subsidiary of BPCE, the second-largest banking group in France. For additional information, please visit Natixis Investment Managers’ website at im.natixis.com.

Stonebridge Investment Counsel, LLC and Natixis are not related entities.