StonebridgeFOCUS | Purposeful Planning Part II

Did you know that the concept of retirement wasn't around until the 1880s?

It wasn't seriously considered until German Chancellor, Otto Von Bismarck, proposed the idea in 1883 before the Reichstag (German Parliament). By today's standards, the Chancellor's forced retirement program at age 65 would be considered a form of ageism. But, it's worth considering why it took so long for retirement to come around.

Prior to the 18th century, the average life expectancy was around 26 to 40 years. It's hard to retire when you're too busy dying of bronchitis or pneumonia. Even by 1883, few lived beyond 65. Remember that penicillin wouldn't be around for another 50 years. Curious that age 65 became a universally accepted age to retire.

Despite the German Chancellor's proposal, retirement wouldn't pick up steam until after the Industrial Revolution. Aging factory workers were reluctant to retire, which created high unemployment among younger workers ready to fill their shoes. These concerns would be exacerbated several decades later in the 1930s. The Great Depression made retirement an economic necessity.

Retirement, as we know it today, became ingrained in the United States with the passing of the Social Security Act in 1935. As part of President Roosevelt's domestic program, the New Deal, the Act created the OASDI (quite literally called Old-Age, Survivor's, and Disability program). This program differs in many ways from Von Bismark's proposal in 1883, but the goal was the same: incentivize retirement. Fast forward another 85 years and we have retirement communities popping up, US golf courses tripling between 1921 and 1930, and the mastery of leisure. Clearly we have come a long way from dying of dysentery in your 30s, but what does retirement look like now?

Here we are, nearly 140 years later, where we've come full circle in reevaluating the efficacy of retirement. Prior to COVID, every week you could find an article published by a financial outlet regarding Boomers' underfunded retirement, or Millennials needing to stop buying avocados and lattes in order to save money. What's interesting is that all those pieces are predicated on the idea that retirement is the same today as it was. It's just not.

When we talk about goals, Retirement is typically one of them. But not in the same way it is perceived or expected it would be since in the 1930s. For most, retirement won't mean hitting the links by 9 am and Early Bird Special at 4 pm. Retirement shouldn't be a date, but a choice. It should be an inflection point where you can confidently make a transition in your life.

In the eyes of the athlete, artists, entertainer, or entrepreneur, there may be no such thing as retirement. There may only be career transition, or the pivot to the next craft or project. Our objective at Stonebridge, is to equip you with the tools and advice to get you to that transition point and confidentially make that decision.

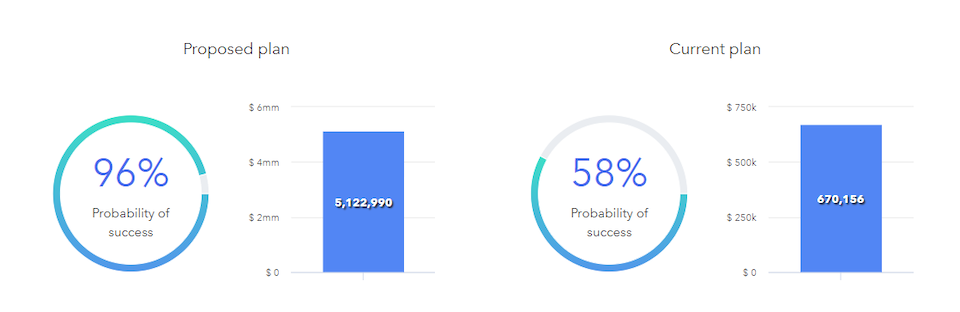

The first step is acknowledging where you are at and identifying where you want to be. Are you on the right path? How confident are you?

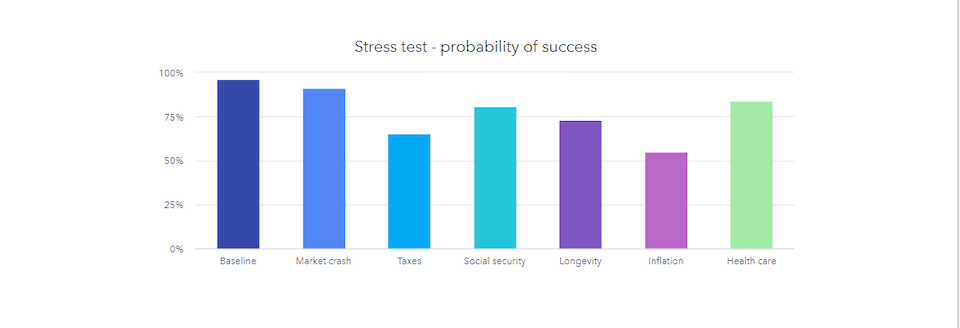

Have you considered what happens if things don't go according to plan? If markets crash? if taxes go up? If the cost of health is higher?

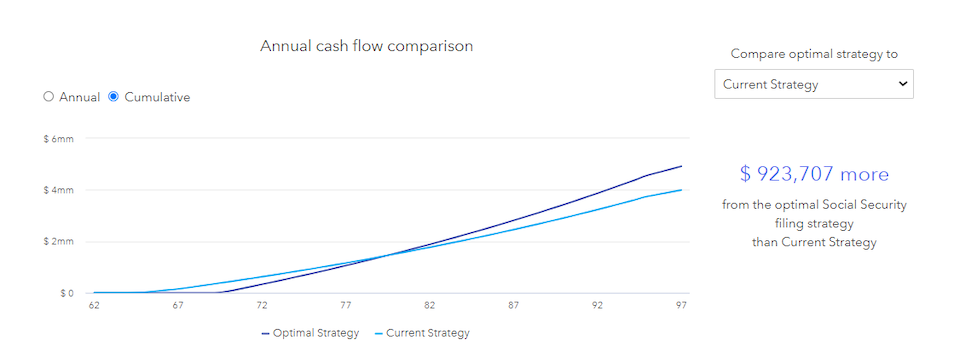

Are all of your resources optimized to help you reach your goals?

If you're approaching career transition or retirement, it's critical to answer these questions. Your team at Stonebridge is well equipped to help create and address these issues with a holistic, actionable plan.

Should you have any questions, feel free to reach out. Thank you for your continued trust and confidence in Stonebridge.

In Part III of the Purposeful Planning series, we will be focusing on asset protection and some of the tools available to protect your wealth.

Best,

Tyler Martin CFP®