Stonebridge Focus - April Showers

The global stock-market recovery that defined early 2019 extended into April. Major developed markets, including the U.S., U.K., Europe and Japan, climbed steadily throughout the month. Emerging markets also gained, but performance diverged in China, with Hong Kong slightly higher and mainland stocks essentially flat after a late-month selloff. Intermediate- and long-term government bond rates generally increased in the U.S., U.K. and eurozone, while short-term rates were mixed, resulting in steeper yield curves. Oil prices advanced for the full month, but peaked in late April before retreating a bit.

Recently, SEI Private Trust Company published their April Monthly Market Commentary entitled, “April Showers More Gains on Equities,” which we thought would be of interest.

Snapshot:

- The global stock-market recovery that defined early 2019 extended into April. Major developed market government bond rates generally increased and oil prices climbed.

- U.S.-China trade talks continued through the end of April—touching on foreign access to Chinese markets, subsidies for Chinese companies, enforcement mechanisms, and whether to remove tariffs erected last year.

- In a world where the best and worst-performing asset classes tend to dominate headlines, it can be easy to forget that diversification has historically been a reliable approach for meeting long-term investment objectives.

U.S. and China trade talks continued through the end of April - touching on foreign access to Chinese markets - with China’s negotiators showing willingness to remove some ownership caps, lower barriers to entry in the financial sector, and allow agreements to apply outside of geographically limited free-trade zones. Subsidies for Chinese companies remained a point of contention, however, since China’s negotiators contend that a complex web of local, regional and country-level development initiatives makes enforcement intractable. Talks also covered whether and how far to remove tariffs erected last year, and mutually agreeable enforcement mechanisms appeared to take shape as talks progressed. A Chinese trade delegation is scheduled to visit Washington, DC beginning on May 8.

Central Banks

The U.S. Federal Open Market Committee began its latest meeting on the last day of April and announced no new policy actions on May 1.

The Bank of England’s Monetary Policy Committee did not meet during April, and voted unanimously on May 2 to abstain from any policy changes. Committee guidance retained a bias toward higher rates in the future, depending on the Brexit outcome.

The European Central Bank’s Governing Council also did not meet to address monetary policy in April, but minutes released from its March meeting showed that some members were interested in extending a hold on rate increases through the first quarter of 2020 (rather than the end of 2019) given a questionable outlook for the eurozone economy, although this did not come to pass.

The Bank of Japan held monetary policy steady in April with a zero percent target for the ten-year Japanese government bond. It lowered the inflation target for 2020 and overall economic growth projections for 2019 and 2020.

Economic Data

U.S. manufacturing activity expanded at a measured pace in April, while services sector growth slowed. Inflation, as measured by the core personal consumption expenditures price index—the Federal Reserve’s (Fed) preferred measure—continued to edge lower in March, touching 1.6% year over year. The U.S. economy grew at a 3.2% annualized rate during the first quarter, surpassing the fourth quarter and handily beating expectations.

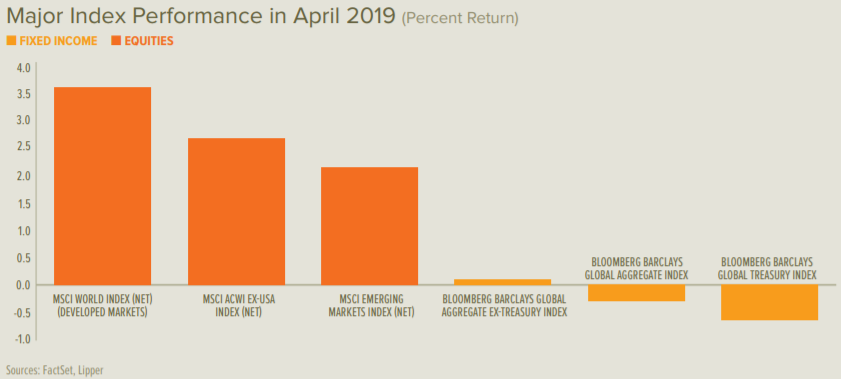

Major Index Performance

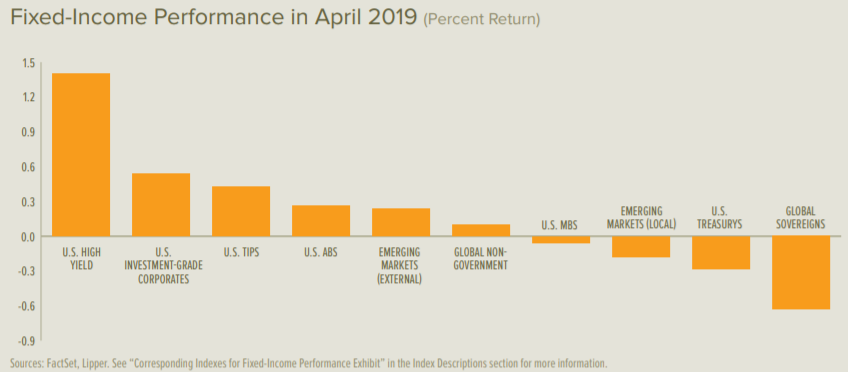

Fixed-Income Performance

Our Point of View

Today, there’s no denying that a synchronized global growth slowdown is underway. However, it does not mean that the world economy is in recession or that it will soon fall into one. China and the U.K., for example, are the second and fourth worst-performing countries, according to the Organisation for Economic Co-operation and Development’s composite leading indicators. Yet China continues to post gross domestic product growth in the vicinity of 6%, while the U.K. recorded an increase of 1.3% last year (both in inflation-adjusted terms).

The spread between 3-month and 10-year U.S. Treasurys briefly went negative in March after narrowing throughout much of the expansion. Recession historically occurs within 12 to 18 months of the yield curve either narrowing to 25 basis points or inverting. The only time recession did not follow a yield-curve inversion was in the 1966-to-1967 period—although U.S. economic growth slowed dramatically.

Deeper recessions usually cause sharper share-price declines (as was the case in 1973). More expensive stock markets (as seen following the 1998- to-2000 tech bubble) also are more vulnerable. But the time between an initial yield-curve inversion and the emergence of a bear market can be extremely long. The Fed’s change in rhetoric at the start of the year certainly has been a helpful catalyst in sparking the risk-asset rally and credit-spread narrowing. By stressing patience and data dependence, the U.S. central bank signaled that the pace of U.S. interest-rate increases will slow considerably from that of the past two years. The Fed’s decision makers approvingly noted that the benefits of the long economic expansion are finally being distributed more evenly as the labor market tightens; they seem confident that the economy can grow without generating worrisome inflationary pressures, even as most measures of labor-market activity point toward accelerating wage inflation.

We see plenty of opportunities in emerging equities as investors gain confidence that the worst is behind us for the asset class. But a sustained improvement depends on better global growth. In our view, China is the linchpin; we are optimistic that the country’s economic conditions will improve as it begins to feel the lagged impact of easier economic and monetary policies.

The plunge in risk assets during the fourth quarter and subsequent bounce back in the first quarter of this year is a reminder that one should always expect the unexpected when it comes to investing. Cash was king in 2018, providing a 2.1% return, according to the ICE BofAML USD 3-Month Deposit Offered Rate Constant Maturity Index. However, cash was consistently one of the worst performers in most other years going back to 2009. Emerging equities fell at the other end of the performance spectrum in 2018—the MSCI Emerging Markets Index sustained a total-return loss of 14.6%—but was the strongest category in 2017 and posted a double-digit return in 2016.

In a world where the best- and worst-performing asset classes tend to dominate the headlines, it can be easy to forget that diversification has historically been the most reliable approach for meeting long-term investment goals—especially when looking through the lens of risk-adjusted returns.

“I think the single most important thing you can do is diversify your portfolio.”

- Paul Tudor Jones, an American investor, hedge fund manager and philanthropist.

To learn more about our distinctive goals-based approach to life and wealth management or request a copy of the full-length monthly commentary paper, please do not hesitate to contact our team directly.

We look forward to continuing to provide useful insights and relevant solutions focused on helping you achieve your greatest financial potential.

Thank you for your continued trust and confidence in Stonebridge.

All the best,

Mitch

About SEI Private Trust Company

Now in its 50th year of business, SEI (NASDAQ:SEIC) is a leading global provider of investment processing, investment management, and investment operations solutions that help corporations, financial institutions, financial advisors, and ultra-high-net-worth families create and manage wealth. As of Dec. 31, 2018, through its subsidiaries and partnerships in which the company has a significant interest, SEI manages, advises or administers $884 billion in hedge, private equity, mutual fund and pooled or separately managed assets, including $307 billion in assets under management and $573 billion in client assets under administration.