StonebridgeFOCUS - The Beauty of Diversification

At the end of a busy week for earnings, investors are taking stock of both good and bad corporate surprises and parsing the details of the first-quarter gross domestic product report. U.S. GDP expanded at a 3.2 percent annualized rate in the January-March period, according to Commerce Department data Friday that topped all forecasts in a Bloomberg survey. However, underlying demand was softer than the headline number indicated, with weak consumer spending and a gauge of inflation coming in below policy makers’ target.

Recently, SEI Private Trust Company published their Quarterly Market Commentary entitled, “Markets Rebound Around the Globe,” which we thought would be of interest.

Snapshot:

- Investor sentiment took a 180-degree turn in the New Year. Stock markets rallied around the globe through most of the first quarter, reclaiming much of the fourth quarter’s losses.

- The U.S. and China continued to negotiate the terms of a trade agreement after President Donald Trump’s administration waived an early March deadline to impose tariffs in the absence of a deal.

- In a world where the best and worst-performing asset classes tend to dominate headlines, it can be easy to forget that diversification has historically been a reliable approach for meeting long-term investment objectives.

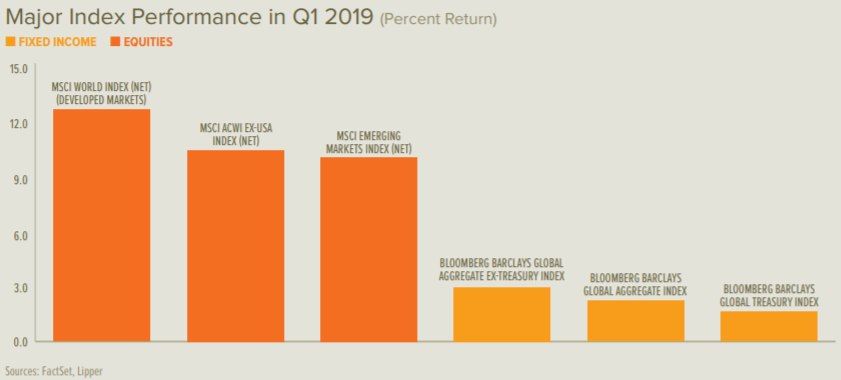

Investor sentiment took a 180-degree turn in the New Year. Stock markets rallied around the globe through most of the first quarter, reclaiming much of the fourth quarter’s losses. The S&P 500 Index delivered its best quarterly performance since 2009. West Texas Intermediate crude oil topped $60 per barrel at the end of the three-month period after climbing by more than 30%.

Government bond rates declined in the U.S., U.K. and eurozone during the first three months of the year. The U.S. Treasury yield-curve inversion continued to deepen over the quarter, with the yield on the 10-year Treasury ultimately falling below those of Treasurys with the shortest maturities. Long-term rates generally fell by more than short-term rates in the U.K. and eurozone, while German 10-year government bond yields dropped back below zero.

The U.S. and China continued to negotiate the terms of a trade agreement after President Donald Trump’s administration waived an early March deadline to impose tariffs in the absence of a deal. China’s negotiators provided assurances toward the end of the quarter that foreign companies will have greater access to Chinese investments. U.S. negotiators promoted the idea of retaining a portion of the U.S. tariffs imposed on $250 billion of Chinese products last year as leverage to ensure China’s compliance with the terms of the eventual agreement. A second summit between Trump and North Korea’s Supreme Leader Kim Jong Un faltered in February when they failed to strike a compromise on steps toward North Korean denuclearization in exchange for sanction relief.

On the domestic front, the U.S. government remained partially shuttered for most of January due to an impasse between Congress and the White House about whether to fund a multi-billion dollar wall on the U.S.-Mexico border championed by the president. The Trump administration received a measure of resolution in March, when the special counsel investigating the 2016 election reportedly “did not establish that members of the Trump campaign conspired or coordinated with the Russian government” to sway the election (although it did concur with the U.S. intelligence community’s assessment that Russia sought to influence the outcome in Trump’s favor). The special counsel also reportedly did not conclude that the president committed criminal obstruction of justice (but neither did it exonerate him); leadership at the Department of Justice found insufficient grounds to establish obstruction of justice charges based on the special counsel’s report. Congressional Democrats intend to obtain and review the special counsel’s report to make a separate determination in conjunction with information gathered through Congressional investigations.

The original Brexit Day (March 29) came and went without fanfare, as the EU granted an extension to the U.K. in hopes of avoiding a no-deal departure. Prime Minister Theresa May’s deal was defeated in Parliament three separate times during the quarter—even as May offered to resign in exchange for votes in support of her deal—as were additional options that legislators debated and voted upon in late March (and again on April 1). These measures included a customs union between the U.K. and EU (which failed by only three votes in the second session) and a second referendum (which failed by only 12 votes in the second session). May’s bid to resign in exchange for parliamentary support generated speculation about a change in leadership; separately, likelihood of a general election increased because the impasse risks provoking a no-confidence motion. Regardless, unless there is an immediate resolution, the U.K. is expected to participate in the EU’s elections later this spring.

Central Bank

The Federal Open Market Committee took a dovish turn during the quarter, with new economic projections that showed zero interest-rate increases in 2019. It also unveiled a plan to start slowing the reduction of its balance sheet in May—before halting reduction altogether in September and converting its allocation of mortgage-related assets to Treasurys.

Economic Data

U.S. manufacturing conditions oscillated between modest and healthy growth during the quarter, while services sector activity showed firmer strength. In February, the unemployment rate declined to 3.8% and the labor-force participation rate increased; more Americans joined or returned to the labor market amid an increase in average earnings. The U.S. economy expanded by a 2.2% annualized rate during the fourth quarter, propelled by strong consumer spending.

Our Point of View

Today, there’s no denying that a synchronized global growth slowdown is underway. However, it does not mean that the world economy is in recession, or that it will soon fall into one. China and the U.K., for example, are the third and fourth worst-performing countries, according to the Organisation for Economic Co-operation and Development’s composite leading indicators. However, China continues to post gross domestic product growth in the vicinity of 6%, while the U.K. recorded an increase of 1.3% last year (both in inflation-adjusted terms).

The spread between 3-month and 10-year Treasurys went negative in March after narrowing throughout much of the expansion. Recession historically occurs within 12 to 18 months of the yield curve either narrowing to 25 basis points or inverting. The only time recession did not follow a yield-curve inversion was in the 1966-to-1967 period—although U.S. economic growth slowed dramatically.

Deeper recessions usually cause sharper share-price declines (as was the case in 1973). More expensive stock markets (as seen following the 1998- to-2000 tech bubble) also are more vulnerable. However, the time between an initial yield-curve inversion and the emergence of a bear market can be extremely long. The Federal Reserve’s change in rhetoric at the start of the year certainly has been a helpful catalyst in sparking the risk-asset rally and credit-spread narrowing. By stressing patience and data dependence, the central bank signaled that the pace of interest-rate increases will slow considerably from that of the past two years.

The Fed’s decision makers approvingly noted that the benefits of the long economic expansion are finally being distributed more evenly as the labor-market tightens; they seem confident that the economy can grow without generating worrisome inflationary pressures, even as most measures of labor-market activity point toward accelerating wage inflation.

The plunge in risk assets during the fourth quarter and subsequent bounce back in the first quarter of this year is a reminder that one should always expect the unexpected when it comes to investing. Cash was king in 2018, providing a 2.1% return. However, cash was consistently one of the worst performers in most other years going back to 2009. Emerging equities fell at the other end of the performance spectrum in 2018—the MSCI Emerging Markets Index sustained a total-return loss of 14.6%—but was the strongest category in 2017 and posted a double-digit return in 2016.

In a world where the best- and worst-performing asset classes tend to dominate the headlines, it can be easy to forget that diversification has historically been the most reliable approach for meeting long-term investment goals—especially when looking through the lens of risk-adjusted returns. While a diversified portfolio rarely wins from one year to the next, it also rarely loses—and therein lies its beauty.

“Successful investing takes time, discipline and patience.” - Warren Buffett

To learn more about our distinctive goals-based approach to life and wealth management or request a copy of the full-length paper, please do not hesitate to contact our team directly.

We look forward to continuing to provide useful insights and relevant solutions focused on helping you achieve your greatest financial potential.

Thank you for your continued trust and confidence in Stonebridge.

All the best,

Mitch

About SEI Private Trust Company

Now in its 50th year of business, SEI (NASDAQ:SEIC) is a leading global provider of investment processing, investment management, and investment operations solutions that help corporations, financial institutions, financial advisors, and ultra-high-net-worth families create and manage wealth. As of Dec. 31, 2018, through its subsidiaries and partnerships in which the company has a significant interest, SEI manages, advises or administers $884 billion in hedge, private equity, mutual fund and pooled or separately managed assets, including $307 billion in assets under management and $573 billion in client assets under administration.