StonebridgeFOCUS – Investment Taxes: Don’t Ignore the Tail

There are many in the financial community who believe taxes shouldn’t drive investment decisions. Fund managers pursuing active strategies, for example. For many of them, the primary objective is to generate pretax alpha, giving less thought to the after-tax consequences. Maybe this works for them. After all, there are trillions of dollars invested in actively managed funds, so clearly people are buying what they’re selling. “We never let the tax tail wag the investment dog,” one of those managers told Barron’s earlier this year.

Recently, Parametric Portfolio Associates published a Research Commentary entitled, “Investment Taxes: Don’t Ignore the Tail,” which we thought would be of interest.

Snapshot:

- In 2018, US large-cap equity funds lost 6.3% on average last year, according to Morningstar, investors got stuck paying an additional 3% to 4% in taxes as a result of the distributions.

- Not only did SMA holders avoid the 3–4% tax drag experienced by investors in actively managed funds, but they would likely have been able to generate anywhere from 1% to 5% in additional tax benefits from tax-loss harvesting the individual stocks in their portfolio.

- The variation in the tax benefit depends on how highly appreciated one’s holdings are, but the impact is undeniable.

We have nothing against actively managed funds, of course, or any other vehicle that delivers value to its investors. However, many managers and investors could improve their returns by paying more attention to taxes. As we’ve shown in research, and in our work with business managers and their high-profile clients for over 16-years, investment taxes do matter. In fact, they matter a lot. And 2018 proved it once again.

Market Volatility in 2018: Insult Meets Injury

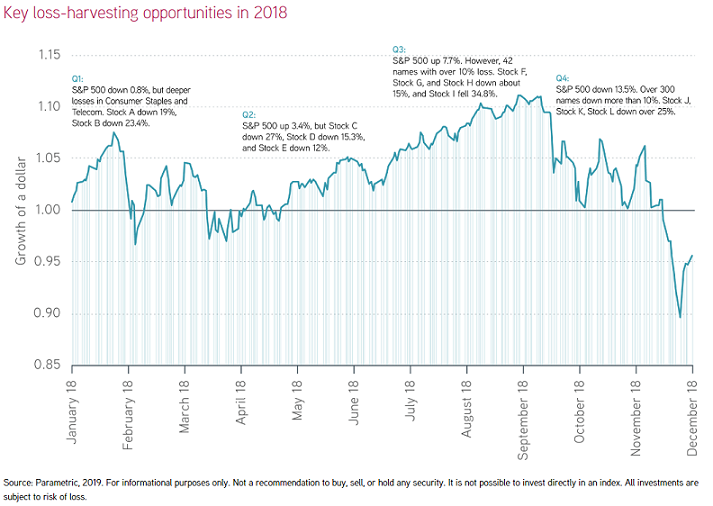

Not that you need reminding, but 2018 saw some periods of extended market volatility—perhaps most notably in the fourth quarter, when the S&P 500® Index lost more than 13.5% of its value. That swoon helped the index close the year down nearly 4.4%.

So on the performance front, not great news. But wait—for many fund investors, there was some insult to go along with that injury. As the Wall Street Journal reported in November, funds’ capital gains distributions were putting 2018 on track to be the costliest year ever in terms of investor tax exposure. Sure enough, data from Morningstar confirmed this, with US equity funds distributing an average of 10.6% of their net asset value in gains in 2018, mostly the result of funds’ being forced to sell off highly appreciated assets to make up for redemptions as investors continued to switch from actively managed funds to index funds.

As a result, even though US large-cap equity funds lost 6.3% on average last year, according to Morningstar, investors got stuck paying an additional 3–4% in taxes as a result of the distributions (depending, of course, on the investor’s tax rate). What could they have done differently?

Tax-Advantaged Investment Vehicles

Unlike actively managed funds, ETFs are passive, with low turnover. This makes them inherently tax efficient, and so ETF investors likely received no capital gains distributions for them in 2018. But ETFs are also a single, unified investment product, preventing investors from accessing the individual underlying securities that make up the fund. So if a stock lost significant value during one of the periods of volatility we saw in 2018—and 75% of the stocks in the S&P 500® had a maximum drawdown of more than 20% at some point during the year—there was no way to sell that stock without liquidating one’s holdings in the entire ETF.

Investors in separately managed accounts (SMAs), on the other hand, do have access to the individual underlying securities in their portfolio. This enables stock-level tax-loss harvesting—something SMA asset managers can do for their clients throughout the year, whenever opportunities present themselves. This is helpful not just when the market falls but also when it’s broadly up yet individual stocks or sectors fall. The chart below illustrates a few examples from last year.

The upshot? Not only did SMA holders avoid the 3–4% tax drag experienced by investors in actively managed funds, but they would likely have been able to generate anywhere from 1% to 5% in additional tax benefits from tax-loss harvesting the individual stocks in their portfolio. The variation in the tax benefit depends on how highly appreciated one’s holdings are, but the impact is undeniable.

Our point of view

It’s neat and easy to think of investment tax as the tail of the dog. However, we think that metaphor is barking up the wrong tree. Instead we think it’s more accurate to describe tax as the tail of the crocodile. Sure, it’s still a tail, but on that ancient beast the tail represents 40% or more of its total body. And when the tail moves, the entire animal moves. In investing, as in nature, we ignore the tail at our peril.

“One of the most serious problems in the mutual fund industry, which is full of serious problems, is that most mutual fund managers behave as if taxes don’t matter. But taxes matter. Taxes matter a lot.”

David F. Swenson, an American investor, endowment fund manager, and philanthropist. He has been the chief investment officer at Yale University since 1985.

To learn more about the primary drivers of tax efficiency in our SMA solution(s) or request a copy of the full Research Commentary, please do not hesitate to contact our team directly.

We look forward to continuing to provide useful insights and relevant solutions focused on helping you achieve your greatest financial potential.

Thank you for your continued trust and confidence in Stonebridge.

All the best,

Mitch

About Parametric

Parametric Portfolio Associates LLC (Parametric) uses investment science to build and manage systematic investment strategies and to implement custom portfolio solutions providing clients with targeted investment exposures with control of costs and taxes. Based on principles of intellectual rigor, ingenuity and transparency, Parametric seeks to deliver repeatable client outcomes with consistently high levels of service and maximum efficiency. As of December 31, 2018, Parametric managed $216.6 billion in assets on behalf of institutions, high-net-worth individuals and fund investors. Headquartered in Seattle, Parametric also has offices in Minneapolis, Westport, Connecticut, Boston, and Sydney, Australia. For more information, visit parametricportfolio.com.

When Stonebridge decided to introduce an overlay portfolio management solution to its investment process, we chose to work with Parametric and SEI Private Trust Company. In the firm’s 2010 paper, Tax Efficient Investing in Theory and Practice, Parametric presented many of the concepts that now form the basis of Stonebridge’s tax alpha strategy; the added value by reducing taxes on an investment portfolio.