StonebridgeFOCUS | The Financial Foundation (Ages 4-11)

What was your first memory of money? I was probably around seven or eight years old when my mom created this elaborate chore-based system. My sister and I would earn marbles which would be used to fill up a plastic Tupperware® container. Every time we filled up the container, we were rewarded with a random activity. It could be going out to lunch with dad or making a trip to the Dollar Store®. I don’t know if you can really call that a “money memory”, but it’s certainly the first money-related memory I can recall.

Both personal responsibility and financial literacy are developed primarily between the ages of 5 and 18[i]. In the best of circumstances, parents can foster development of their children’s personalities, healthy money beliefs, and capable money skills for adulthood between these ages. That is the financial foundational period in a child’s life, as learning has a compounding effect. If the foundation isn’t strong, subsequent layers will crumble or fail to take hold. This isn’t to say that older kids can’t be taught, just that the hill is a steeper climb.

Everyone says that having kids is a big responsibility, which is certainly true, but there are two things they don’t tell you. First, that you’ll be watching the same Youtube® video on repeat for the next four years. And second, a lot of the ways that you learned financial lessons as a kid are no longer effective or don’t apply to today’s world.

The exponential growth in technology has reshaped how we educate and prepare next-gen. If you’re a parent, chances are that online banking wasn’t around when you opened your first checking account. You probably used a check registry to track spending. There was no ApplePay®, PayPal®, or Venmo®. Certainly, there were no chip readers or digital wallets. The world has changed and is changing more quickly. The financial lessons we learned are still important, but the way we learned them no longer applies.

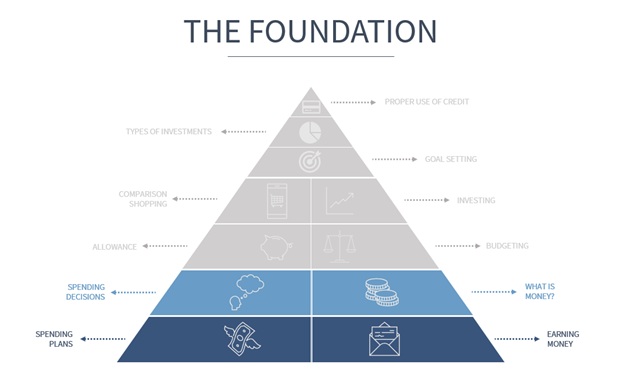

The four cornerstones of a strong financial foundation include:

- Defining what money is and what it isn’t

- Making wise spending decisions

- Developing spending plans

- Learning how to earn money

Defining money is one of the newer challenges parents face. Between virtual currency earned in video games to cryptocurrencies, it’s an increasingly complicated landscape. Digital gameplay and “earning” virtual currency on Candy Crush has changed how kids interact with real money. What’s the danger? Last year a 6-year old racked up $16,000 in expenses from the Apple Store, all from in-app purchases for Sonic Forces (which is a game, I had to google it).

Today, only a ¼ of all transactions are done in cash[ii], and if we overlay age demographics, it’s probably safe to say that cash transactions will continue to plummet. Even though we are in the midst of a migration away from cash, money needs to be made real to kids. Using coins and bills keeps money tangible and allows them to differentiate the real stuff versus gamified, online experiences.

Making wise spending decisions is developed by reinforcing rational behavior patterns. Parents can teach this by making kids practice decision making in structured situations. These structured situations could be as simple as having a child spend play money for food items or exchanging money for toys they want. These activities help kids analyze simple alternatives without major negative consequences while gaining self-confidence in the decision-making process.

Developing a spending plan introduces structured spending decisions and a precursor to budgeting. Notice that this is a spending plan. We are only focusing on one part of the equation. This is primarily because most financial pitfalls can be avoided by simply controlling spending, rather than trying to find additional income sources to meet unsustainable spending. In developing a spending plan, kids should be introduced to three of the five money categories: “spend”, “save”, and “share” (we’ll introduce “earn” and “invest” later).

Learning “spend” and “share” are natural for most kids, but the “save” category is typically more challenging, especially due to societal influences and desire for instant gratification. Working to develop a strong “save” habit will pay dividends when kids grow up and are able to obtain their first credit card. Improper use of credit is one of the most common financial mistakes, and usually originates from an inability to save effectively.

Learning how to earn money completes the second part of the budgeting equation. As adults, we go to work and earn money to provide for our family’s needs and wants, but children may not easily see or make the connection that work leads to money. Early training in earning small amounts of money demonstrates how work and money are connected. This is a fine line, because kids should perform certain tasks at home just because they are part of the family. But doing additional tasks to earn money for their spending plans distinguishes between shared responsibilities as a family member and responsibilities that earn them money.

I don’t think anyone has ever uttered the phrase, “finance can be fun!” Let’s face it, some of the things we do for our kids aren’t necessarily fun but are an investment in their future. We take them to the dentist. We try to make sure they get enough exercise and eat healthy. All good things. By starting to build a strong financial foundation at a young age, it will be far easier for kids to develop more skills to avoid financial pitfalls and setbacks.

At Stonebridge, our job isn’t just to help our clients accomplish their personal life and wealth goals or achieve their greatest financial potential, but also to empower them to become confident and fearless investors. In our view, this means providing resources to prepare you and the next gen for multigenerational wealth that is only sustainable when the lines of communication are open and a strong financial foundation is cemented.

If you’d like more information or additional financial literacy resources for younger children, please feel free to reach out and we’d be delighted to assist. Here are a couple of freebies for coin and bill denominations:

Cash Puzzler | Target ages 3-6 for learning different bills.

Peter Pig Game | Target ages 5-8 for learning different coins.

Happy Teaching,

Tyler Martin, CFP®, CPWA®

[i] Gallo and Gallo 2002, Hausner 2005, Godfrey 2003.

[ii] Federal Reserve Bank of San Francisco