StonebridgeFOCUS | Maximizing Resources (Ages 15-22)

Trading stocks is so easy today. You can download Robinhood® in about 30 seconds. In less than five minutes you can link a bank account and start trading meme stocks or crypto. Very different than my first stock purchase. I’m not that old, but sometimes it feels that way.

I bought my first two stocks at the same time in 2010. Netflix and Evcarco Inc. I’m sure you’ve heard of at least one of these. It probably took me two hours to figure out how to open a brokerage account and fund it. The only reason I spent that much time on it was because I had just decided to change my college major from History to Finance. Buying my first stocks felt like something a Finance major would do. Netflix’s stock price closed around $25 a share that year. Evcarco’s stock price was under $0.01. You probably can see where this story ends.

As a poor college student, $25 was a lot for me. I got nervous seeing the price fluctuate and sold Netflix quickly but held on to the “value” I got with Evcarco. Over the last year, Netflix’s share price has hit nearly $700. And Evcarco, well, they’re bankrupt (Full disclaimer, I still have Evcarco in my account just to serve as a helpful reminder to avoid emotionally driven financial decisions).

But this story isn’t another one of those articles that starts with “If you just invested $10,000 in X company 10 years ago” blah blah blah. It’s about how technology has made trading easier than ever but hasn’t fixed our behavioral biases or how we sometimes make irrational decisions about money.

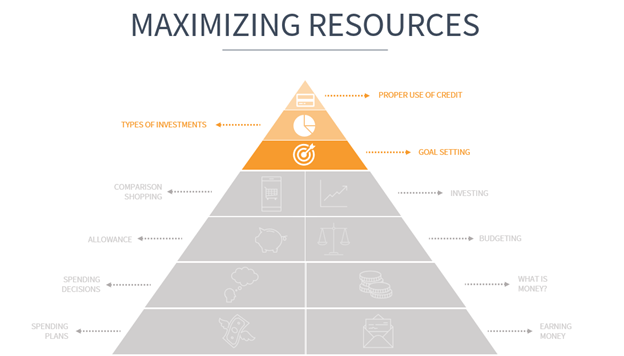

It’s really hard to avoid making those mistakes. One of the best ways to recognize and combat your own biases (or your child's) is to create a strong financial foundation, layer it with constructive behaviors, and emphasize maximizing resources.

Now that the foundation has been set and behaviors built, the focus should shift to maximizing resources by exploring:

- Goal setting

- Types of investments

- Proper use of credit

Goal setting is effectively next level budgeting. You’ve managed your expenses. You’ve started to save. The next logical question is what are you saving for? Financial goal setting should be a four-part process.

Step 1 – Be realistic.

Step 2 – Be specific.

Step 3 – Have a timeframe.

Step 4 – State the action that needs to be taken to accomplish it.

Follow these steps and goals (both big and small) and it will get accomplished.

Types of investments probably haven’t been thoroughly discussed at this point. Kids should have been exposed to stocks, but likely don’t have a strong grasp on bonds, mutual funds, exchange traded funds (ETFs), real estate, etc. What is more likely is that they’ve been exposed to more high-risk, YOLO-type investments (such as crypto, NFTs, and meme stocks). Platforms like Robinhood® have meaningfully changed the investing landscape and introduced investing to a younger demographic. While that’s certainly something to celebrate, the problem is it has also increased destructive trading behaviors.

There is more than ample evidence demonstrating that when individual investors trade frequently, they significantly underperform[i]. There’s nothing wrong with taking some speculative bets. But that’s not a strategy. It doesn’t lead to long-term success. Just get on base. Take the walk. Hit singles. Swinging for fences may work on occasion, but usually leads to a strikeout.

Stress the fundamentals of investing: compounding, patience, and diversification. (Did you know that if you doubled a penny every day for 31 days you would have over $10 million? Crazy right!?!). But keep things interesting by talking about companies that kids know. Consider their favorite restaurants, clothes, or technologies.

The point of the exercise isn’t to ensure the investment is a guaranteed home run (after all, there is value in learning about loss), the point is to get them to understand how investing and markets function in a healthy setting. The longer these lessons are put off, the larger the stakes become for their financial success. A good starting point is setting up a virtual portfolio (See resources below).

Proper use of credit is an underappreciated but powerful skill. Responsible use of credit is more than just seeking the lowest interest rate on a mortgage or car loan. Employers are increasingly pulling credit reports of potential employees as a part of their hiring process. In the past, adding a child as an authorized user on a credit card was the primary way parents helped build their child’s credit history. While this certainly can be beneficial, it’s not without drawbacks.

A small balance on your credit report might be a major red flag on your child’s credit report (high debt to income), which might hurt them when applying for their own loan. This can also be problematic if you haven’t educated them on proper use of credit. In the end, you may just be giving them the ability to support unhealthy or reckless spending patterns.

Instead, consider using a secured credit card which is equivalent to bowling with bumpers. Secured credit cards require deposits that act as collateral. Let them build their own credit, while learning low risk lessons along the way.

Another credit-related pitfall is borrowing too much. If your kids need to borrow, encourage them to keep total debt (excluding housing) less than 20% of their income and monthly payments lower than 10%.

As kids age and start becoming contributing members of society, the learning shouldn’t stop. As kids mature, they should be kept aware of the family values and goals that will ultimately determine whether generational wealth will be sustained or depleted. Every family has a preferred and healthy level of disclosure. You don’t need to run through the whole balance sheet, but effective communication can help prevent what many parents fear: frivolous spending of an inheritance. And while legal instruments, like trusts, are an outstanding option for providing some measure of control, there is only so much you can do from the grave.

Morgan Housel writes, “one of the most important financial skills is getting the goalpost to stop moving. It’s also one of the hardest.” If we can teach the next generation to keep their expectations from growing past their income, that should cover a lot of the financial pitfalls faced by the next-gen.

At Stonebridge, our job isn’t just to help our clients accomplish their personal life and wealth goals or achieve their greatest financial potential, but also to empower them to become confident and fearless investors. In our view, this means providing resources to prepare you and the next gen for multigenerational wealth that is sustainable because the lines of communication are open, a strong financial foundation cemented, constructive behaviors built, and resources maximized.

If you’d like more information or additional financial literacy resources for adult children, please feel free to reach out and we’d be delighted to assist. Here are a couple of freebies that cover a variety of areas:

How The Market Works | 100% free virtual stock market simulation that allows students to practice investing before using real money.

Reality Check | An online calculator that shows students how much income is needed when they are on their own to support the lifestyle they want. Students fill out a checklist of lifestyle choices, including shelter, food, etc. Reality Check tells them how much income and education are needed & lists a few jobs that fall in the desired pay scale.

Happy Teaching,

Tyler Martin, CFP®, CPWA®

[i]The Journal of Finance | Trading is Hazardous to Your Wealth