Turn Down for What

Raise your hand if you remember Y2K. If you don’t, let me give you a little back story.

Y2K, short for "Year 2000," refers to a computer bug that was expected to potentially cause widespread problems when the new millennium began on January 1, 2000. The concern arose because many computer systems and software at the time represented years using only the last two digits (e.g., '99' for 1999, '00' for 2000) to save memory and storage space. As a result, there was a fear that when the year rolled over from '99 to '00, computers might interpret it as the year 1900 instead of 2000. The fear over collapsing computer systems led to widespread concerns ranging from a financial collapse, air traffic disruptions, food shortages, to utility and infrastructure failures. Do you know what happened on January 1, 2000? Nothing. Absolutely nothing.

So why are we all sitting around waiting for a recession when it’s not going to happen?

{kind=link}

For the last 18 months, we’ve all heard that we are “in a recession,” “entering a recession,” “on the cusp of a recession,” “a recession is on the horizon,” or something similar. Spoiler: a recession hasn’t materialized. To be fair, there was perfectly reasonable evidence to support that take. In the last 70 years, the US has not experienced an inflation rate over 9% without going into a recession. Interest rates were rising. The housing market was slowing. Credit was tightening. History was on the side of the recession. But like all of us waiting for the world to end because of a silly computer bug, nothing has happened.

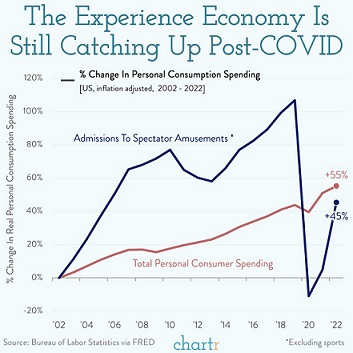

When evaluating the last year, there are several reasons we can point to explain why we haven’t experienced a recession. What first comes to mind is the resiliency of the American consumer.

About 70% of the US economy is consumer spending (i.e. going to Taylor Swift concerts, taking the fam to Applebee’s, and sipping watered down cocktails on a Carnival Cruise), and consumer spending is still strong. It certainly helps that Jeff Bezos made up a shopping holiday in the middle of the year to help bolster spending until we get to the Christmas shopping season. Never underestimate Americans ability to spend.

Second, the response we all thought would happen with the Federal Reserve raising rates faster than you can skip YouTube ads, never came to be. Consensus was that higher rates would collapse the housing market, rapidly raise unemployment, and drive down consumer spending. So, what actually happened?

- Consumer sentiment is the highest level since July 2021.

- Unemployment is approaching 50-year lows.

- Labor force participation is closing in on pre-pandemic levels.

- Pay raises are finally outpacing inflation.

- Existing home prices remain stable.

- Active home listings are rising, as is new home construction.

Sure, there was some bank stress that lasted for about 5 minutes earlier this year. But most of the bank stress was related to risk-taking by specific banks (looking at you Silicon Valley Bank).

Mortgage rates have climbed, which has made things particularly difficult for first homebuyers. But new home construction should provide a pathway to homeownership. Suffice to say, businesses and consumers continue to navigate a higher cost and interest rate environment surprisingly well.

There are two ways this recession narrative could play out.

- We move into a new growth cycle and we kindly forget that 75% of economists were calling for a recession as recently as last December. Between economists and weatherman, I don’t know who gets more room to be wrong.

- We eventually have a recession, it has to rain eventually, and there will an uproar of “I told you so’s.”

I’m keeping my feet planted in 1. Until we start to see evidence of an economic downturn, let me remind you of the wise words of 20th century wordsmith Jonathan H Smith (colloquially known as Lil Jon of the Eastside Boyz) who said, “Turn Down for What.”

It’s easy to be pessimistic because it comes across as expertise. It’s harder to be optimistic because it comes across as naïve. It’s better to be realistic. The glass is not half full. It is not half empty. It is at 50%.

Thank you for your continued trust and confidence.

Tyler Martin, CFP®, CPWA®