StonebridgeFOCUS | The American Spendthrift Part I

Never play monopoly. This is an important lesson I learned last year over the holidays with my in-laws. The first few rounds are always the same. Accumulate property. Build. Repeat. Occasionally go to jail. But as the game drags on, wealth becomes concentrated, players file bankruptcy, and rules become flexible. Before I knew it, I’m still playing monopoly, but my father-in-law and wife were building some sort of Parker Brothers conglomerate by consolidating their real estate holdings.

It’s all in good fun, but a helpful reminder that sometimes, we aren’t all playing the same game. In this two-part series, we will evaluate the current spending in Washington, its impact on national debt, and repercussions that may follow.

Deficit spending can be defined by the amount of money spent that exceeds income over a particular period of time. If you were reviewing your own budget, deficit spending would be those little red numbers at the bottom of the page indicating that you’ve spent too much on Amazon and Caramel Frappuccinos. In the case of the United States, instead of online retail and trips to the coffee shop, spending is on defense, education, healthcare, and a multitude of other services and programs.

Deficit spending has always been contentious in the world of economics. English economist John Maynard Keynes became increasingly popular after the Great Depression, driven by his philosophy on government intervention during financial crises. As part of his economic autopsy, Keynes argued that the depth and duration of the Great Depression would have been less severe if governments intervened and pumped money into the economy, thereby stimulating demand. If you’re thinking, “Hey, isn’t that what’s happened over the last 18 months?”, then you’re right.

There has been plenty of handwringing and finger pointing in Washington over deficit spending, debt ceilings, national debt, yada yada yada. Despite the “controversy”, our elected officials haven’t stopped running deficits for 78 of the last 92 years. Republican or Democrat, we can all unite around our commonality: we’re spendthrifts.

The budget proposal recently released by the Biden Administration for discretionary spending (just the things the President gets to pick) totals $1.52 trillion for 2022. Notably, that does not include mandatory spending for interest payments on debt or entitlement programs, which makes up about two thirds of all spending.

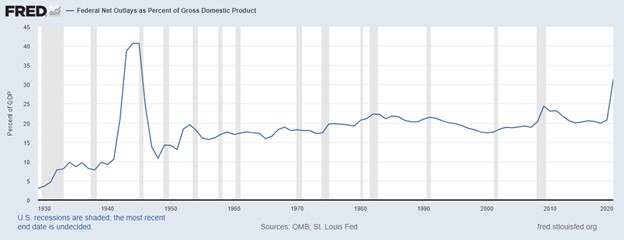

Last year, the federal government spent over 31% of GDP (gross domestic product), which has only been higher in the peak of WW2 (40% in 1944-45). In laymen’s terms, the government spent nearly a third of the total wealth created in the country last year. But this isn’t an indictment on a particular president or administration. This is about how we impose our financial beliefs into something that plays by an entirely different set of rules.

Regardless of what future spending looks like, we still need to address the trillion(s) dollar elephant in the room that would even make Dr. Evil blush. Specifically, $6 trillion in stimulus since last April, another $2+ trillion on the way in the form of an infrastructure package, and more in the form of tax reform (recently announced American Families Plan).

So what happens to the deficit? How do we pay for all this stuff?

When the government spends more than it brings in, it will typically issue bonds to match the deficit. Those bonds can be bought by its Central Bank (read: Federal Reserve, or Fed) which make their way into the hands of individual investors, retirement plans, other governments, mutual funds, etc. With interest rates staying at historically low levels, using “cheap” bonds to pay for these deficits seems attractive. Consider how enticing 0% financing looks when buying a new car, or mortgages under 3%. It’s probably fair to say that most of us took advantage of low interest rates over the past few years to buy new stuff or refinance our existing stuff.

After maxing out our credit in WW2, the debt that accumulated was never paid down or paid off in the same way that people pay off loans and mortgages. The bonds used to pay for the first two world wars were just replaced with new bonds. The US economy effectively grew its way out of deficit spending. Money was cheap (low interest rates) and pent-up demand (soldiers returning from war) were the two ingredients needed for explosive growth. The economy grew faster than the debt.

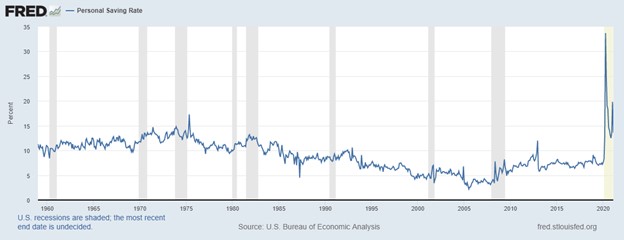

Flash forward to today and people are saving money at levels not seen since the post-WW2 era (low interest rates and stimulus) with signs of pent-up demand (reopening of the economy after a year of lockdowns). The groundwork is laid for a similar style recovery, however, just because something worked or was true yesterday, doesn’t mean that it is true today.

It’s fair to look at the national debt and be pessimistic, even concerned. But if you view debt and deficits through the lens of a government, which doesn’t have an expiration date, there never really is a payoff date, just minimum payments on the credit card. A card credit with an interest rate of less than 2%.

Perhaps the reason we fear deficits and debt, is because the average person can’t do what most governments can. When the average person runs out of money, the options are far more punitive. Credit cards, pay-day loans, or distributions from retirement plans can create a hole that’s nearly impossible to dig out of. In the case of managing income and expenses, the government has one key advantage over the rest of us: time.

Governments, like corporations, are not born with expiration dates. Governments are not saving for retirement or vacation homes. There won’t be a day when Uncle Sam calls it quits, moves to Boca Raton, and starts collecting his pension. Time is on the government’s side and they can do things that the average person cannot. Specifically, spending money well beyond their current income, or deficit spending.

As of January, the average interest rate on all outstanding government debt is hovering around 1.6%. Apart from zero percent financing at your local Audi dealership, there probably isn’t a better deal out there.

If we acknowledge that there is no future pay off, or date that all the bills come due, then what really matters is just the interest. Debt servicing, or the interest payments on debt, are part of that mandatory spending mentioned earlier. In dollar-terms, it sounds like a lot (close to $350 billion). But it accounts for about 8.5% of total revenue or income. For comparative purposes, the average American household spends 12% of their income on interest each year.

I do want to take a moment and point out that there’s no underlying suggestion that people should be making minimum payments on credit cards and follow the same approach. On the contrary, carrying credit card debt is a sure-fire way to go nowhere in building wealth. But something I’ve learned about life in general is to always know what game you are playing and that others may be playing an entirely different game with an entirely different set of rules.

This isn’t to say that deficit spending does not have consequences. Applying Newton’s third law, where every action has an equal and opposite reaction, it’s fair to say that there are probable repercussions to running deficits. Particularly, over extended periods of time. But notice what element is missing from Newton’s third law…time. The law doesn’t say “equal, opposite, and immediate” reaction. Time is missing. Which makes the concept of a “Debt Clock” all the more ironic.

The problem with measuring the consequences of debt and deficit spending is that we don’t immediately know or see them. In fact, the economic repercussions can move at a glacial pace that, over a period of years or decades, can go missed entirely. Most economists suspect that sustained deficit spending leads to higher inflation and higher taxes. Maybe. That’s the tidy, intuitive, and rational response. But the world we occupy isn’t that. It’s chaotic, counterintuitive, and irrational.

In Part II of our series, we’ll explore the repercussions of deficit spending, the plans the Biden Administration has for taxes, and why inflation isn’t what we think.