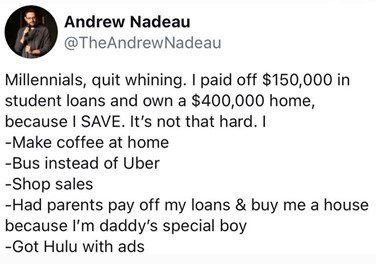

I don’t have a lot of pet peeves. But if you tell me that Frappuccinos® are what holds back Millennials from financial freedom, I’ll throw down.

I don’t have a lot of pet peeves. But if you tell me that Frappuccinos® are what holds back Millennials from financial freedom, I’ll throw down.

What was your first memory of money? I was probably around seven or eight years old when my mom created this elaborate chore-based system. My sister and I would earn marbles which would be used to fill up a plastic Tupperware® container. Every time we filled up the container, we were rewarded with a random activity. It could be going out to lunch with dad or making a trip to the Dollar Store®. I don’t know if you can really call that a “money memory”, but it’s certainly the first money-related memory I can recall.

Both personal responsibility and financial literacy are developed primarily between the ages of 5 and 18[i]. In the best of circumstances, parents can foster development of their children’s personalities, healthy money beliefs, and capable money skills for adulthood between these ages. That is the financial foundational period in a child’s life, as learning has a compounding effect. If the foundation isn’t strong, subsequent layers will crumble or fail to take hold. This isn’t to say that older kids can’t be taught, just that the hill is a steeper climb.

Did you know that twins have a higher rate of left-handedness? About 22% are southpaws compared to only 10% of singletons. Also, about 40% of twins develop their own language to communicate with one another. My wife and I are only weeks away from welcoming our twin boys into the world, and despite how close we are to the due date, the reality hasn’t really set in. I haven’t really thought much about their future interests, passions, or even what they will look like. I think about how I am going to prepare them for a world that no one can fully understand, or for a world that will be very different than today. I think about statistics and numbers, like cost of daycare, cost of college, and family wealth transfers. Approximately 90% of wealth doesn’t survive three generationsi. As the saying goes, “shirtsleeves to shirtsleeves.”

I’m probably the furthest thing from a fashionista, or someone who keeps up with the latest fashion trends. I like things that are practical and sensible. Good gas mileage, socks as Christmas gifts, and I understand the appeal of cargo shorts. Just this past week in our office, we were talking about convertible pants or the ones with a zipper at the knee. I’ve been told that those are not fashionable. But in the spirit of Fashion Week, I think there are some ideas we can glean from fashions and fads and how they relate to investing.

In fashion, there appears to be three main categories: 1) Staples or timeless classics, 2) fads (styles that have seasons which come and go), and 3) things that never should have happened. Anyone remember male rompers, also referred to as RompHims? Again, I’m no fashion expert, but I think these would qualify as “things that should’ve never happened.” (You can still find them on Amazon. You’re welcome). I think these same three categories can be applied to investing.