StonebridgeFOCUS | What Are the Side Effects

In the 1950s, Upjohn Company developed a drug called Minoxidil, which was designed to treat ulcers, among other conditions. It turns out the drug wasn’t very good treating ulcers, but it had an unexpected side effect: hair growth. By the late 1980s, the drug that was designed to treat ulcers and high blood pressure brought us Rogaine®. Certainly not what the Upjohn Company had in mind, but a benefit to society, nonetheless. Unfortunately, side effects (of the medical or economic variety) don’t always have a positive outcome.

Let’s consider the last twenty years of financial and economic history.

In 2001, the Federal Reserve cut interest rates after the dot com bubble which helped create the housing bubble. The housing bubble led us into a financial crisis that created a poor labor market. Tens of millions decided to seek a college degree to the tune of nearly $2T[1] in student loans with a 10.8% default rate.[2]

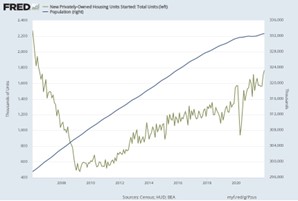

Burned from the housing bubble, real estate development dropped considerably from over 2.2 million homes being built each year in 2006 to less than 1.7 million in 2021, despite the US population increasing by 35 million over that time frame.[3]

A pandemic forced a global economic shut down creating significant supply chain kinks, which led to massive government stimulus that injected $3.7T[4] into the economy and to the Fed cutting interest rates (again), which led to setting the housing market on fire (again). All of which contributed to rising inflation. So, what does the Fed do? Raise interest rates which will likely lead into recession.

Some economic side effects pop up relatively quickly, like the inflationary pressures we are experiencing in 2022. Others can take a decade (i.e. today’s housing market). What is unique about economic side effects is that a negative effect for one person can be a positive for another. Rising interest rates are certainly welcomed by income-seeking investors. However, rising interest rates also means borrowing money that is more expensive, which directly impacts potential homebuyers.

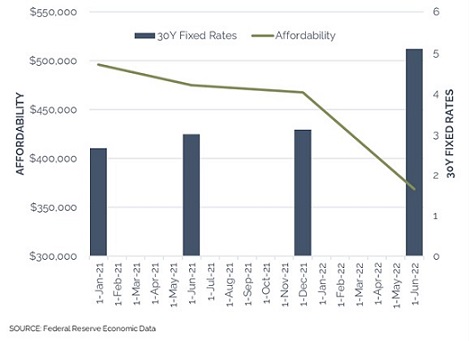

Let’s say you were looking to buy a home last year and could afford a $2,000 monthly mortgage payment. In 2021, you could afford a $500,000 home. In 2022, due to rising rates, you could only afford a $368,000 home. Throw in reduced inventory, competition from hedge fund and private equity buyers, and more costly building materials and you have one of the most challenging real estate markets imaginable.

It’s impossible to know the unintended consequences of the current market and economic climate. There will certainly be side effects we feel immediately and those that go unnoticed for years and years. Uncertainty tends to compel us to action, even if it is to our own detriment. Here are a few things that can keep you from self-inflicted financial wounds.

Have a plan. The importance of having an investment policy (or plan) in place cannot be overstated. A thoughtful plan that keeps you on track and focusing on your specific life and wealth goals can help drown out the noise.

Have patience. The economy and markets move in cycles and difficult environments pass. We have seen this time and time again. We’ve navigated wars, pandemics, and crisis after crisis. This too shall pass.

Have a partner. A sounding board or a safe space to vent is a constructive measure for expressing concerns, fears, and frustrations. Your financial team should help equip you to be a more confident and fearless investor through education as well as providing a complete picture of financial markets and economy.

At Stonebridge, we are fully committed to the success of our clients and trusted partners by ensuring that achievement-based plans are in place, and that we provide the resources necessary to become a fearless investor.

Thank you for your continued trust and confidence in Stonebridge.

Tyler Martin, CFP®, CPWA®

[1] Educationdata.org

[2] Educationdata.org

[3] Federal Reserve Economic Data

[4] USASpending.gov